The Consumer Financial Protection Bureau is finalizing its proposal to extend until October 1, 2022 the mandatory effective date of the new Qualified Mortgage definition based largely on a loan’s annual percentage rate (the “APR-Based QM”). For applications received prior to that date, lenders seeking to make QMs may opt for either the original QM

A QM Freeze in the Forecast

The CFPB announced today that it expects to propose a rule to delay the July 1, 2021 date to comply with the new Qualified Mortgage (“QM”) rule.

The CFPB’s statement provides that the extension would allow lenders more time to make QM loans based on their debt-to-income ratio (and Appendix Q), or based on the

Will the CFPB Freeze the GSE QM Patch?

Since the Inauguration on January 20th, the Biden Administration has busily issued orders to reverse certain policies of the prior administration. In customary fashion upon a change in political parties in the White House, President Biden’s Chief of Staff also sent a memorandum to executive departments and agencies to consider postponing pending rulemakings to allow review by the new slate of policymakers. Among those rules are two Qualified Mortgage (“QM”) Rules of the Consumer Financial Protection Bureau (“CFPB”).

New White House Chief of Staff Ronald Klain’s memorandum specifies that for rules that have already been published or issued but have not yet taken effect, the agencies must consider postponing the rules’ effective dates for 60 days from the date of the memorandum (i.e., until March 21, 2021). If the agency postpones the effective date, the agency must consider opening a 30-day period for interested parties to provide more comments. The memorandum then instructs those agencies to consider whether even further delays are appropriate.

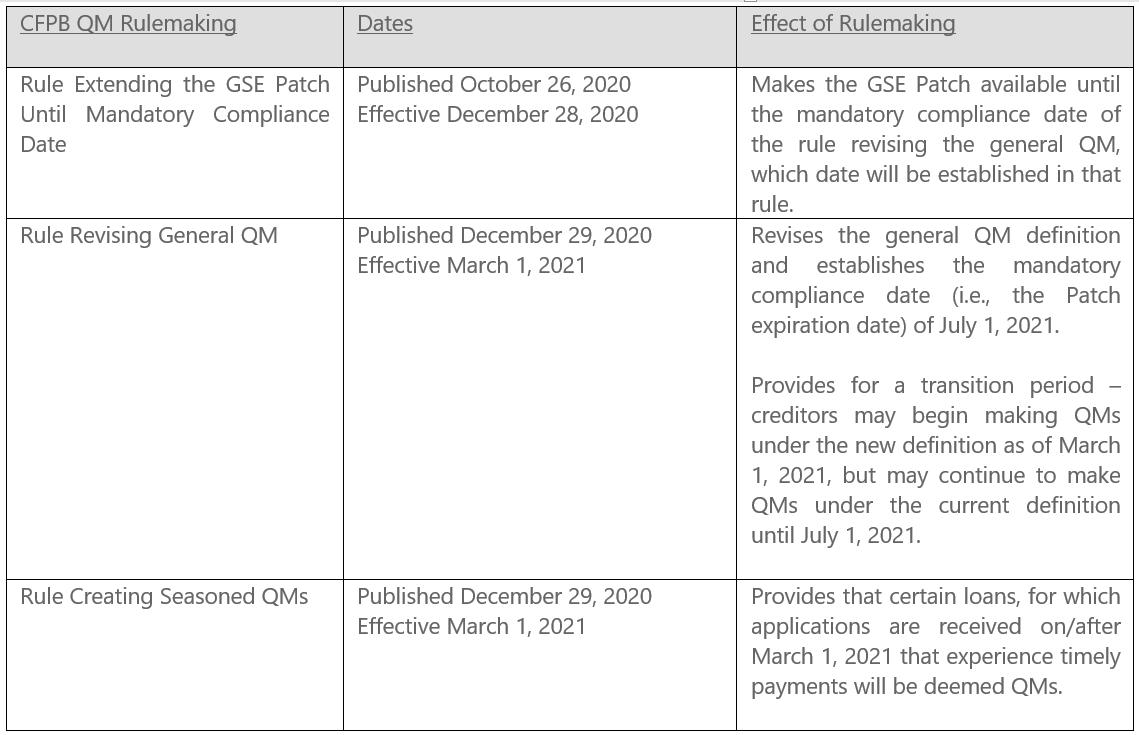

Speaking of engaging interested parties, the CFPB has been reconsidering QM issues for years. The agency has been spurred by a statutory requirement to assess and report on the 2013 QM Final Rule, as well as the January 10, 2021 expiration date of the special QM category for loans eligible for purchase by Fannie Mae or Freddie Mac (the so-called “GSE Patch”). In all, over the course of several years, the CFPB has reportedly received more than 680 comments on QMs from creditors, industry groups, consumer advocacy groups, elected officials, and others. In response to that input, the CFPB issued a final rule extending the GSE Patch until the “mandatory compliance date” of a separate final rule that would revise the general QM category (or until the GSEs emerge from conservatorship), essentially erasing that looming GSE Patch expiration date. Then the CFPB issued two other final QM rules – one to revise the general QM definition and establish that mandatory compliance date, and one to create a seasoned QM category for certain mortgage loans that experience a period of timely payments.

In comparing the effective dates of those rulemakings to the White House’s January 20th memorandum, one can see that the CFPB successfully eliminated the January 2021 GSE Patch expiration date, because that rule became effective before the memorandum. However, the other two rules – which establish the Patch’s new expiration date/Mandatory Compliance Date (July 1, 2021), the new definition of QMs, and the seasoned QM – could get caught in the Biden Freeze.

Continue Reading Will the CFPB Freeze the GSE QM Patch?

CFPB Issues New QM Definition and Seasoning Provisions

The Consumer Financial Protection Bureau (“CFPB”) issued two relatively welcome surprises yesterday. First, along with ditching a debt-to-income ratio (“DTI”) ceiling, the agency expanded its proposed general Qualified Mortgage (“QM”) to include loans up to 2.25 percentage points over the average prime offer rate. Mortgage lenders can opt in to the new QM as early as 60 days after the rule is published (so, likely by late February 2021), although compliance becomes mandatory July 1, 2021. Second, the CFPB will begin allowing loans to season into a QM after 36 months of timely payments, so long as the loan is not sold more than once (and is not securitized) during that time.

The CFPB otherwise recently issued a separate final rule, confirming once and for all that the GSE Patch – a temporary QM category for loans eligible for purchase by Fannie Mae or Freddie Mac – would expire on the mandatory compliance date of the agency’s rule revising the general QM definition. Since 2014, in general terms, a closed-end residential mortgage loan could only constitute a QM if the borrower’s DTI did not exceed 43%, or if the loan were GSE-eligible. As the GSE Patch’s expiration date (January 10, 2021) loomed, the CFPB promised to rethink the 43% DTI requirement and provide for a smooth and orderly transition to a post-Patch QM. In considering the public comments it received, the CFPB decided to loosen up on a couple of its proposals.

Specifically, the new general QM and its compliance protection will apply, under the final rule, to a covered transaction with the following characteristics:

- The loan has an annual percentage rate (“APR”) that does not exceed the average prime offer rate (“APOR”) by 2.25 or more percentage points;

- The loan meets the existing QM product feature and underwriting requirements and limits on points and fees;

- The creditor has considered the consumer’s current or reasonably expected income or assets, debt obligations, alimony, child support, and DTI ratio or residual income; and

- The creditor has verified the consumer’s current or reasonably expected income or assets, debt obligations, alimony, and child support.

The final rule removes the 43% DTI threshold and the troublesome Appendix Q.

Continue Reading CFPB Issues New QM Definition and Seasoning Provisions

That’s the Spirit: The Haunting of the CFPB’s GSE Patch

On October 20, 2020, the Consumer Financial Protection Bureau (the Bureau) issued a final rule extending the Government-Sponsored Enterprise (GSE) Patch until the Bureau’s general qualified mortgage (QM) changes kick in. To keep from spooking the residential mortgage markets, the Bureau’s final rule accomplishes three main objectives:

- Retains the temporary GSE qualified mortgage (QM) safe harbor until compliance with the Bureau’s revised general QM definition becomes mandatory, but without any overlap period as some commenters requested;

- Establishes an implementation period to facilitate the transition to the revised general QM loan definition, and suggests the adoption of an “optional early compliance period” for transitioning to the revised general QM before the mandatory compliance date; and

- Resolves the frightful gap the Bureau’s proposal threatened to create by terminating the GSE Patch in accordance with the date of loan application, as opposed to the date of loan consummation.

For those who have been cowering in the shadows, the GSE Patch refers to a temporary compliance safe harbor the Bureau granted in 2014 for loans eligible for purchase by Fannie Mae or Freddie Mac. Those GSE-eligible loans have been deemed to comply with federal ability-to-repay requirements applicable to closed-end residential mortgage loans. The GSE Patch grants QM status to certain loans excluded by the general QM definition – notably, loans with a debt-to-income ratio that exceeds 43%. The GSE Patch is set to expire on January 10, 2021, or when the GSEs are released from conservatorship, whichever occurs first. The Bureau is otherwise revising its general QM definition, in part to ensure that the Patch expiration does not deprive worthy borrowers of access to credit.

In establishing the end date for the GSE Patch, the Bureau’s final rule first clarifies that there will not be an “overlap period.”

Continue Reading That’s the Spirit: The Haunting of the CFPB’s GSE Patch

Mayer Brown Announces Consumer Finance Licensing Team Transition

Mayer Brown is pleased to announce that Krista Cooley, a partner in our Financial Services Regulatory and Enforcement group, has recently expanded her existing practice to take the lead in managing our state licensing practice. Krista is an experienced Consumer Financial Services attorney with over 19 years of experience. In this role, Krista advises clients on compliance with the requirements of federal and state laws governing the licensing, approvals and practices of brokers, lenders, purchasers and servicers of mortgages and other consumer loan products, as well as sales finance companies, money service businesses and collection agencies. She also assists clients in navigating the complex state and federal licensing and approval process in connection with, among others, new business lines, legal entity conversions, restructuring and change of control transactions.

Stacey Riggin, one of our Government Affairs Advisors, and Dana Lopez, our Licensing Manager, work closely with Krista and will continue to oversee our team of five regulatory compliance analysts, each of whom has over ten years of experience working together on licensing matters. Our team has decades of experience in managing nationwide licensing projects and assisting clients in obtaining approval with state and federal government agencies to engage in a variety of financial services related activities. Our team also coordinates regulatory approvals needed to facilitate mergers, equity investments, stock and asset acquisitions, and servicing sales and transfers.Continue Reading Mayer Brown Announces Consumer Finance Licensing Team Transition

A Coming of Age Story: CFPB Proposal to Allow Seasoned Loans to Grow Into QMs

The Consumer Financial Protection Bureau (CFPB) is proposing to allow a loan to become a Qualified Mortgage (QM) when it grows up. On August 18th, the CFPB issued a proposal that would amend the agency’s Ability-to-Repay (ATR) Rule to provide that a first-lien, fixed-rate loan meeting certain criteria, that the lender has held in its portfolio, could become a QM after 36 months of timely payments. Figuring that if a borrower has made payments on a loan, the lender must have made a reasonable determination of ability-to-repay, the proposal would open the safe harbor door to non-QMs (including those originated as such intentionally or inadvertently) and higher-priced QMs that otherwise receive only a rebuttable presumption of compliance with the Rule. The proposal also would, consequently, close the door on those borrowers’ ability to challenge the lender’s underwriting determination in a foreclosure, which otherwise would last far beyond the three-year period.

Specifically, the CFPB proposes that a covered loan for which an application is received on or after this rule becomes effective could become a “seasoned QM” and earn a conclusive safe harbor under the ATR Rule if:

- The loan is secured by a first lien;

- The loan has a fixed rate for the full loan term, with fully amortizing payments and no balloon payment;

- The loan term does not exceed 30 years; and

- The total points and fees do not exceed specified limits (generally 3%).

In addition, the creditor must have considered the consumer’s debt-to-income ratio (DTI) or residual income and verified the consumer’s debt obligations and income. In alignment with the CFPB’s pending rulemaking revising the general QM definition, the creditor would not have to use the Rule’s Appendix Q to determine the DTI. Also, as indicated above, a loan generally would be eligible as a seasoned QM only if the creditor holds it in portfolio until the end of the three-year seasoning period.

Continue Reading A Coming of Age Story: CFPB Proposal to Allow Seasoned Loans to Grow Into QMs

Federal Housing Agencies and GSEs Announce Updates to COVID-19 Relief Measures for Mortgage Loan Borrowers

In recent weeks, the US federal housing agencies and government-sponsored enterprises (GSEs) that insure, guarantee, or purchase “federally backed mortgage loans” covered by Section 4022 of the CARES Act (Act) have continued their intense pace of issuing temporary measures, and updates to such measures, intended to implement the Act’s provisions applicable to such loans. These

CFPB Hatches a QM Proposal for GSE Patch

As rumored, the Consumer Financial Protection Bureau (“CFPB”) is proposing to revise its general qualified mortgage definition by adopting a loan pricing test. Specifically, under the proposal, a residential mortgage loan would not constitute a qualified mortgage (“QM”) if its annual percentage rate (“APR”) exceeds the average prime offer rate (“APOR”) by 200 or more basis points. The CFPB also proposes to eliminate its QM debt-to-income (“DTI”) threshold of 43%, recognizing that the ceiling may have unduly restrained the ability of creditworthy borrowers to obtain affordable home financing. That would also mean the demise of Appendix Q, the agency’s much-maligned instructions for considering and documenting an applicant’s income and liabilities when calculating the DTI ratio.

The CFPB intends to extend the effectiveness of the temporary QM status for loans eligible for purchase by Fannie Mae or Freddie Mac (the “GSE Patch”) until the effective date of its revisions to the general QM loan definition (unless of course those entities exit conservatorship before that date). That schedule will, the CFPB hopes, allow for the “smooth and orderly transition” away from the mortgage market’s persistent reliance on government support.

Background

Last July, the CFPB started its rulemaking process to eliminate the GSE Patch (scheduled to expire in January 2021) and address other QM revisions. For the past five years, that Patch has solidified the post-financial crisis presence by Fannie Mae and Freddie Mac in the market for mortgage loans with DTIs over 43%. The GSE Patch was necessary, the CFPB determined, to cover that portion of the mortgage market until private capital could return. The agency estimates that if the Patch were to expire without revisions to the general QM definition, many loans either would not be made or would be made at a higher price. The CFPB expects that the amendments in its current proposal to the general QM criteria will capture some portion of loans currently covered by the GSE Patch, and will help ensure that responsible, affordable mortgage credit remains available to those consumers.

Adopting a QM Pricing Threshold

Although several factors may influence a loan’s APR, the CFPB has determined that the APR remains a “strong indicator of a consumer’s ability to repay,” including across a “range of datasets, time periods, loan types, measures of rate spread, and measures of delinquency.” The concept of a pricing threshold has been on the CFPB’s white board for some time, although it was unclear where the agency would set it. Many had guessed the threshold would be 150 basis points, while some suggested it should be as high as 250 basis points. While the CFPB is proposing to set the threshold at 200 basis points for most first-lien transactions, the agency proposes higher thresholds for loans with smaller loan amounts and for subordinate-lien transactions.

In addition, the CFPB proposes a special APR calculation for short-reset adjustable-rate mortgage loans (“ARMs”). Since those ARMs have enhanced potential to become unaffordable following consummation, for a loan for which the interest rate may change within the first five years after the date on which the first regular periodic payment will be due, the creditor would have to determine the loan’s APR, for QM rate spread purposes, by considering the maximum interest rate that may apply during that five-year period (as opposed to using the fully indexed rate).

Eliminating the 43% DTI Ceiling

Presently, for conventional loans, a QM may be based on the GSE Patch or, for non-conforming loans, it must not exceed a 43% DTI calculated in accordance with Appendix Q. Many commenters on the CFPB’s advanced notice of proposed rulemaking urged the agency to eliminate a DTI threshold, providing evidence that the metric is not predictive of default. In addition, the difficulty of determining what constitutes income available for mortgage payments is fraught with questions (particularly for borrowers who are self-employed or otherwise have nonstandard income streams). While the CFPB intended that Appendix Q would provide standards for considering and calculating income in a manner that provided compliance certainty both to originators and investors, the agency learned from “extensive stakeholder feedback and its own experience” that Appendix Q often is unworkable.

Continue Reading CFPB Hatches a QM Proposal for GSE Patch

Self-Employed Borrowers’ Income – Is the Past Necessarily Prologue?

In a new era of double-digit unemployment resulting from the COVID-19 pandemic, it may be tough for a mortgage lender to predict the amount and stability of someone’s income in order to determine qualification for a home loan. Neither past nor even present levels of income may be reliable indicators of income levels going forward, at least in the short run or until the economic dislocations are substantially behind us. That is why Fannie Mae and Freddie Mac (the “government-sponsored enterprises,” or “GSEs”) recently issued enhanced documentation requirements and considerations for verifying and predicting the income of a self-employed applicant for a mortgage loan. While the GSEs’ documentation requirements apply via contract to approved lenders/sellers, whether those requirements will morph into legal requirements under the Dodd-Frank Act’s “ability to repay” requirements is something to watch in the coming months.

Revised GSE Underwriting Requirements for Eligible Loan Purchases

A determination of whether an applicant has the ability to repay a loan from his or her income or assets is a basic component of loan underwriting – as required both by federal (and sometimes state) law, and by a lender’s investors or insurers. In addition, federal regulations prohibit a lender of closed-end residential mortgage loans from relying on any income that is not verified by reliable documentation. Predicting whether that income will continue into the future takes skill when lending to self-employed borrowers under any circumstances, and is particularly tricky during this unique coronavirus economy. The now-waning government stay-at-home orders and other quarantining efforts may or may not have affected a particular borrower’s business operations, and the scale and duration of those effects going forward are difficult to predict.

In response to that uncertainty, on May 28, 2020 Fannie Mae and Freddie Mac issued guidance requiring that self-employed borrowers must submit a year-to-date (“YTD”) profit and loss statement (“P&L”) that reports business revenue, expenses and net income.

Continue Reading Self-Employed Borrowers’ Income – Is the Past Necessarily Prologue?