Since the Inauguration on January 20th, the Biden Administration has busily issued orders to reverse certain policies of the prior administration. In customary fashion upon a change in political parties in the White House, President Biden’s Chief of Staff also sent a memorandum to executive departments and agencies to consider postponing pending rulemakings to allow review by the new slate of policymakers. Among those rules are two Qualified Mortgage (“QM”) Rules of the Consumer Financial Protection Bureau (“CFPB”).

New White House Chief of Staff Ronald Klain’s memorandum specifies that for rules that have already been published or issued but have not yet taken effect, the agencies must consider postponing the rules’ effective dates for 60 days from the date of the memorandum (i.e., until March 21, 2021). If the agency postpones the effective date, the agency must consider opening a 30-day period for interested parties to provide more comments. The memorandum then instructs those agencies to consider whether even further delays are appropriate.

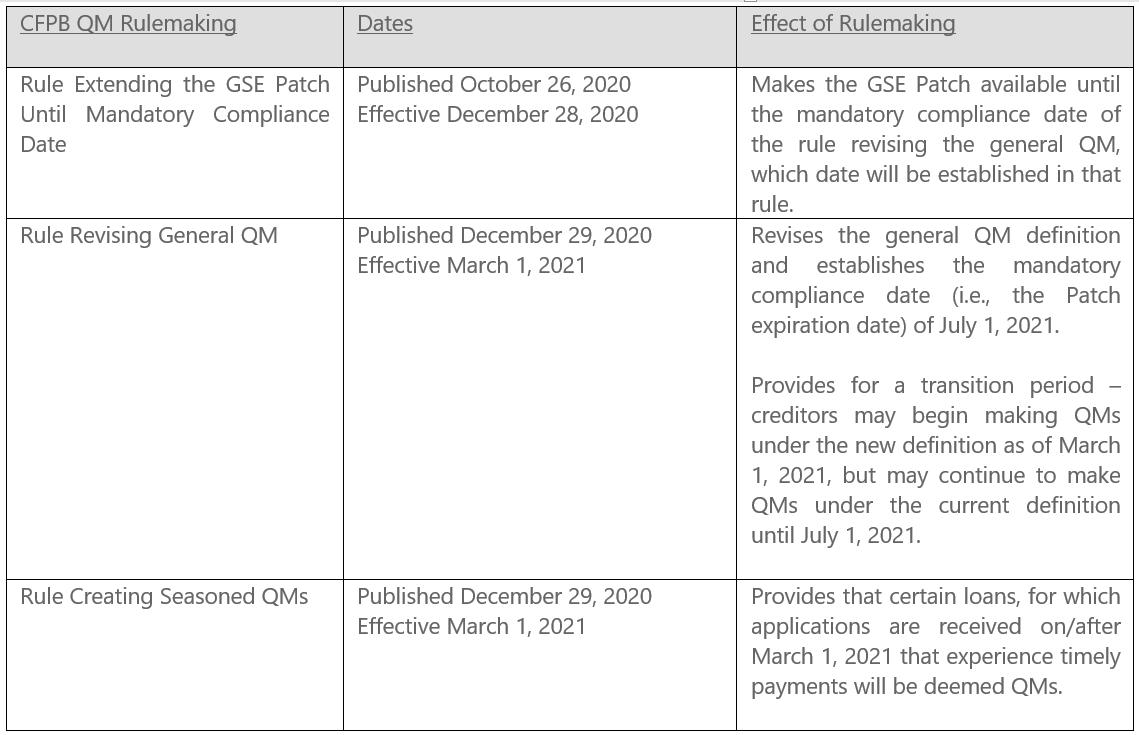

Speaking of engaging interested parties, the CFPB has been reconsidering QM issues for years. The agency has been spurred by a statutory requirement to assess and report on the 2013 QM Final Rule, as well as the January 10, 2021 expiration date of the special QM category for loans eligible for purchase by Fannie Mae or Freddie Mac (the so-called “GSE Patch”). In all, over the course of several years, the CFPB has reportedly received more than 680 comments on QMs from creditors, industry groups, consumer advocacy groups, elected officials, and others. In response to that input, the CFPB issued a final rule extending the GSE Patch until the “mandatory compliance date” of a separate final rule that would revise the general QM category (or until the GSEs emerge from conservatorship), essentially erasing that looming GSE Patch expiration date. Then the CFPB issued two other final QM rules – one to revise the general QM definition and establish that mandatory compliance date, and one to create a seasoned QM category for certain mortgage loans that experience a period of timely payments.

In comparing the effective dates of those rulemakings to the White House’s January 20th memorandum, one can see that the CFPB successfully eliminated the January 2021 GSE Patch expiration date, because that rule became effective before the memorandum. However, the other two rules – which establish the Patch’s new expiration date/Mandatory Compliance Date (July 1, 2021), the new definition of QMs, and the seasoned QM – could get caught in the Biden Freeze.

What does this mean for creditors trying to make QMs (or trying to understand the future scope of the non-QM market)? The Biden Freeze memorandum directs agencies to “consider” postponing the effective date of pending rules; the memorandum does not demand or effectuate an automatic freeze. To date, the CFPB has not announced the results of its consideration. However, if the CFPB were to postpone its December 29th QM final rules, that would likely mean that neither the new general QM definition (with its annual percentage rate threshold) nor the seasoned QM (both of which we discuss here), would become available on March 1, 2021. The current definition of QMs (reliant upon a 43% debt-to-income threshold and the regulation’s strict Appendix Q) would remain in effect. Since the Mandatory Compliance Date is not until July 1st, a relatively brief postponement may not necessarily affect the expiration date of the GSE Patch. However, the new CFPB could consider postponing that date, too, among many other paths the agency could take in response to a new round of public comments.

Careful readers will note that the Biden Freeze memorandum applies to “executive departments and agencies,” but does not provide a definition of those terms to clarify if it applies to independent agencies like the CFPB. As a political matter, however, the agency is likely to follow the Biden Freeze memorandum. Kathy Kraninger, the CFPB Director under the prior administration, resigned on January 20th (and was subject to removal by President Biden in any case). President Biden appointed David Uejio as the CFPB Acting Director and nominated Rohit Chopra to be the permanent Director. It is unlikely those two would push back against President Biden’s directive.

The Biden Freeze memorandum may affect not just the CFPB’s QM rulemakings, but other pending rulemakings by the CFPB and other agencies. For instance, the CFPB issued final rules under the federal Fair Debt Collection Practice Act that are pending effectiveness (scheduled for November 2021). The Administration otherwise appears to be aiming at pending rules of the Department of Labor and the Environmental Protection Agency. While the Administration clearly has many priorities, and the QM Rules have already been subject to several years of consideration and rounds of public input, a new administration may not be able to resist putting its own stamp on as many rules as possible, including putting a freeze on the GSE Patch.