Just two months after financial institutions submitted their so-called “new” data as required under the Home Mortgage Disclosure Act (HMDA), the Consumer Financial Protection Bureau (CFPB) is considering whether to eliminate or revise the requirement to collect and report those new data elements, and whether to change the requirements to report certain business- or commercial-purpose transactions.

Specifically, the CFPB issued an advance notice of proposed rulemaking (ANPR) on May 8, 2019, asking the public for input on those changes. (An agency may issue an ANPR to gather information needed to formulate a proposed rule.) The ANPR fulfills part of the promise announced by former CFPB acting director Mick Mulvaney last year to reconsider nearly all aspects of HMDA reporting, including not just the new data points, but also newly-covered institutions and transactions.

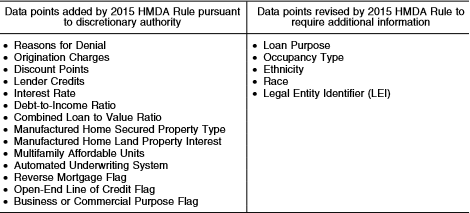

While HMDA (as amended by the Dodd Frank Act) requires certain institutions to collect and report a significant list of data elements regarding the institutions’ home lending activities, the CFPB revised and added to that list during a comprehensive 2015 HMDA rulemaking. Institutions were generally required to report that new data for the first time on March 1, 2019. The 2015 HMDA rulemaking required reporting institutions to implement extensive and costly changes to systems and operations – so extensive that federal regulatory agencies promised to recognize institutions’ good faith compliance efforts, without assessing penalties or even requiring resubmission in connection with errors in the data collected in 2018 and reported in 2019.

The ANPR indicates that the CFPB has heard concerns about the new data elements and the reporting of business/commercial loans. As examples, the ANPR lists the burden of reporting on whether a borrower owns or leases the land on which a manufactured home is located, as that information is not typically gathered during the origination process; and the burden of collecting and reporting disaggregated race and ethnicity categories. The ANPR also explains that the CFPB has heard it can be cumbersome to use the free-form text field for reporting the reasons for loan denial, if the reason is not otherwise on the list. The CFPB also has reportedly heard arguments that loans made to non-natural persons and secured by multifamily property should be excluded as outside of HMDA’s purposes.

Accordingly, the CFPB is requesting the public to identify the “new” data points (listed below) for which the cost of collecting and reporting the information does not justify the benefit of furthering HMDA’s purposes. Those data points are the following:

The ANPR also asks about other factors, if any, the CFPB should consider in connection with proposing to eliminate or revise those data elements; and whether any of them require further explanation.

In addition, the ANPR asks for information regarding:

- The costs, benefits, and possible alternatives for providing information in free-form text; and

- The value, benefits, and burdens associated with collecting and reporting information on business- or commercial-purpose loans made to non-natural persons and secured by multifamily dwellings.

Comments on the ANPR are due by July 8, 2019.